Cooperatives have a long history in Indonesia and were once hailed as the backbone of the people’s economy. Today, however, they risk slipping into irrelevance, even as similar institutions in Singapore flourish and adapt to modern demands.

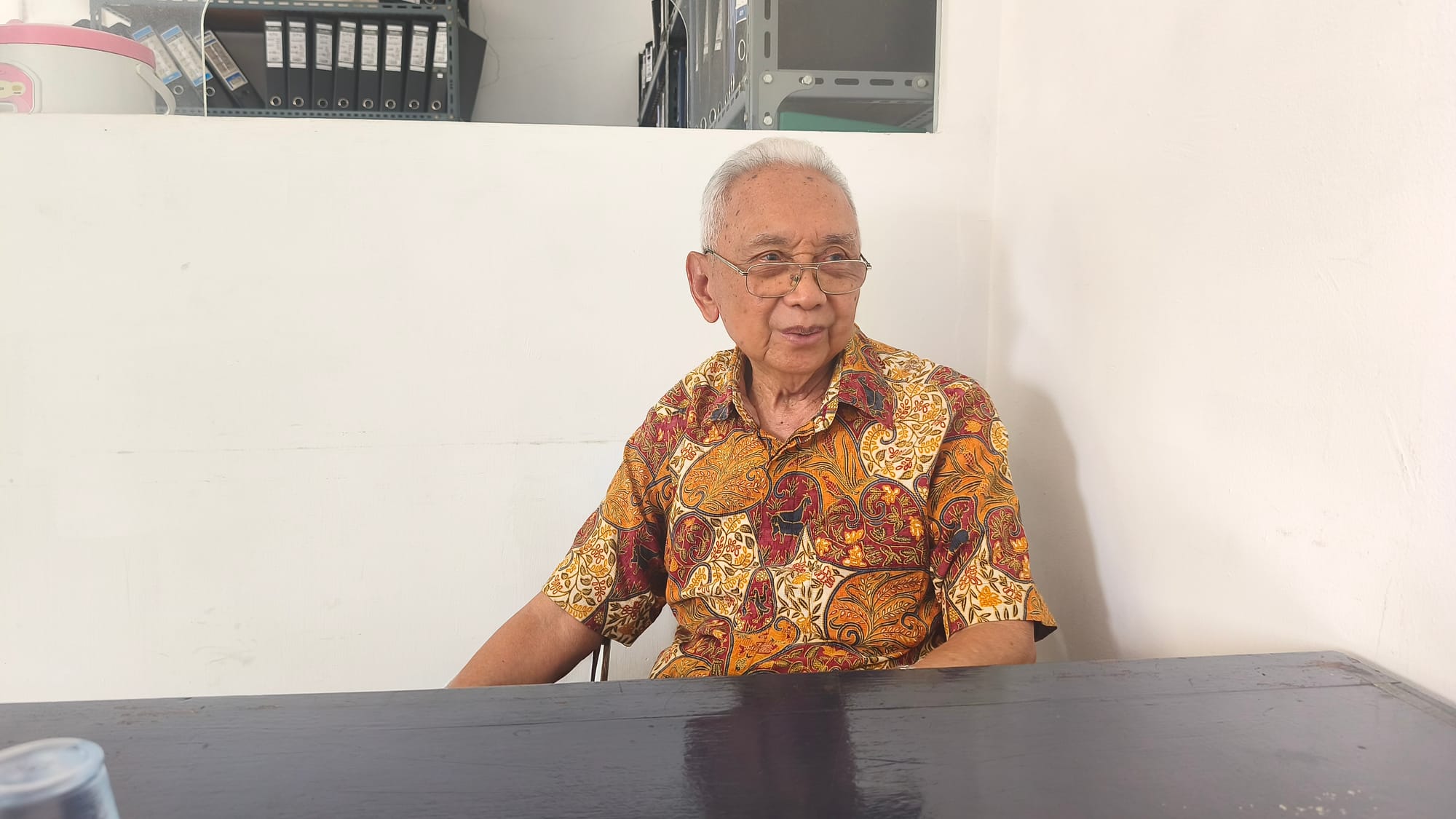

On a Thursday afternoon in late July, Achmad Saubari Prasodjo had just returned from midday prayers when he received SUAR at his three-story office in Jati Padang, South Jakarta. Settling into his desk, the cooperative leader reflected on the challenges facing a sector once central to Indonesia’s economic vision.

For nearly half a century, Achmad Saubari has worked here, at a cooperative that sells a wide variety of goods, ranging from snacks, canned and bottled drinks, and medicines, to frozen meat.

While sipping coffee from his tumbler, the 85-year-old recalled the beginnings of Koperasi Sejati Mulia, which was first established in 1978. At that time, several residents of Jati Padang agreed to form a small business entity.

“It all started from the awareness to help one another,” Achmad said. The founders came from diverse backgrounds—civil servants, private employees, and small entrepreneurs—yet mutual cooperation became the foundation.

The cooperative’s first office was a wooden hut, formerly a project post for a housing complex under construction. Contractors once used it to store building materials before the complex was built, and even the local administration had used it. From this small and humble place, Koperasi Sejati Mulia began to grow.

The cooperative’s first office was a wooden hut, formerly a project post for a housing complex under construction.

Initially, the cooperative’s business line focused only on savings-and-loan services among members and nearby traders. Typically, vegetable sellers would come in the morning to request loans. They would repay them according to agreed terms. “If their goods sold well, they could repay the same afternoon,” Achmad said.

Although the cash turnover was not large, this model proved effective in driving the cooperative’s growth. The 1990s became a pivotal decade for Koperasi Sejati Mulia.

As profits improved, the cooperative purchased a building from the Ministry of Agriculture through a bank loan. The house was large enough and was immediately converted into the cooperative’s office, which it still occupies today. “Now, the BCA and BRI bank buildings next to this office belong to the cooperative. They rent them from us,” Achmad explained.

Once Thrived in Its Time

Today, Koperasi Sejati Mulia manages three business lines. First, savings and loans, continuing the cooperative’s original activity. Second, rental of buildings, rooms, and land.

The cooperative’s second floor is rented out to anyone in need of space, while the parking lot is leased to street vendors. Third, retail trade.

The cooperative’s store sells goods from two sources: homemade cakes and chips produced by members are displayed alongside products supplied by vendors. This blend adds a distinct character to the cooperative’s retail business.

Achmad admits that, in terms of price and product variety, the cooperative cannot compete with major retailers like Alfamart, Indomaret, or Family Mart, which operate nearby. Still, he insists this does not mean the cooperative is bound to lose. He stresses the importance of member loyalty: “We must shop here—this belongs to us together. The profits will come back to us too.”

“We must shop here—this belongs to us together. The profits will come back to us too.”

Membership now stands at around 2,400 people, spread across Jati Padang, Pasar Minggu, and some retirees who have relocated. The membership fee has increased from Rp10,000 to Rp30,000 in line with the cooperative’s growth and expanded facilities.

The organizational structure consists of a chairman, treasurer, and unit managers. Business units—savings and loans, retail, and rental—are managed by the board. Daily decisions are discussed weekly, while major policies are decided at the Annual Members Meeting (RAT), where the cooperative also determines how Surplus Results of Operation (SHU) are distributed among members.

Eroded by Time

In 2017, Koperasi Sejati Mulia reached its peak, recording an annual net profit of Rp1.7 billion. With strong earnings and additional bank loans, the cooperative purchased a building across the street, now rented to an electronics store. The plan was to reinvest rental income into other business units.

Unfortunately, the pandemic disrupted all those plans. “Revenue collapsed. To this day, our bank debt remains unpaid,” Achmad said.

The pandemic disrupted all those plans.

Yet, despite the crisis, Achmad claims no employees were laid off. Though salaries were reduced, he ensured that every worker still received their rights.

Even now, he admits the cooperative’s finances have not recovered. Since 2022, the cooperative has not distributed SHU to members, a moment they eagerly await each year. “The cooperative is still losing money today, not to mention the ongoing installments and operating costs,” Achmad explained.

One of the most logical steps to rescue the cooperative, he said, is to sell the rental building. The board and members have been asked to offer the property, priced at Rp11 billion.

Despite these struggles, Achmad remains hopeful: “Fortune can come from anywhere,” he said, emphasizing that the cooperative must be managed with honesty and discipline.

Despite struggling, Achmad still believes the cooperative he leads will endure.

He firmly rejects informal or unrecorded lending practices, especially when done by board members leveraging their position.

At his advanced age, Achmad also hopes for leadership regeneration. Having served as chairman for more than one term, he believes it is time for younger generations to take over management of this 47-year-old cooperative. “It’s unfortunate, but not many young people are willing to take on this responsibility,” he said.

The members’ trusted savings and loan cooperative.

Much like the story of Koperasi Sejati Mulia in Jati Padang, Koperasi Bina Sejahtera was also founded in 1978 and continues to operate today.

It began as a small rotating savings group (arisan) regularly held by migrants from Gunungkidul, Yogyakarta. They were civil servants, market workers, and self-employed individuals who pooled money to help one another. From those gatherings, the idea of forming a cooperative emerged.

Two years later, in 1980, the cooperative officially obtained legal status. Its 18 founders were mostly long-time Gunungkidul residents living in Cipinang Melayu. At first, the cooperative did not have its own place. Management moved from one location to another, from schools to community halls.

The land and building later associated with the cooperative were originally listed as a grant. But upon review, all acquisitions had actually been made with official receipts. The management then decided to process the property deed under the cooperative’s name—determined not to leave behind problems for future generations.

In its heyday, the cooperative had as many as 647 members, spread across various housing complexes in Cipinang Melayu. “We never delete membership numbers, even if the member has passed away,” said Sulistiono, head of credit. Members came from diverse backgrounds and actively participated in cooperative activities. Today, however, active membership has shrunk to just 57 people.

From the beginning, its core activity was savings and loans. Funds collected from members were lent back for daily needs or small business capital. The cooperative also briefly managed public payphone services and daily credit for vendors.

During the 1990s, they partnered with the tofu-tempeh producers’ association and opened a grocery store. “There was no Indomaret back then—we were the busiest shop,” recalled Sri Sulastri, Chairwoman of Koperasi Bina Sejahtera.

The store became a local staple, selling sugar, flour, and oil sourced from the tofu-tempeh association at affordable prices.

The store was once the community’s go-to before minimarkets began to spread.

As supermarkets and retail chains grew around the neighborhood, the cooperative’s store gradually lost customers, and revenues fell sharply. “We tried managing it ourselves, but ended up with losses,” said Sutrisno, who oversees bookkeeping.

Eventually, the management returned to the old model: 60% of the store is managed by external parties, while 40% remains cooperative-owned.

The cooperative’s survival now rests on a strict savings-and-loan system. Loans are capped at three times the total of members’ principal, mandatory, and voluntary savings, ensuring funds remain safe and revolving. “If your savings are Rp500,000, you can borrow at most Rp1.5 million,” explained Sri Sulastri.

But not all loans are repaid. Some members default due to job loss, moving out, or even online gambling addiction. “Once, someone couldn’t repay and said, ‘Just kill me then.’ What can you do? You feel even less able to collect,” Sulistiono said with a laugh.

To minimize risk, the cooperative now only accepts permanent residents of Cipinang Melayu as members. Renters are not allowed to join, as the management fears they might disappear without repaying debts.

Still, there are success stories. Several home contractors once borrowed hundreds of millions and repaid in full. “We look at who pays regularly and consistently—that’s the capital,” said Sri Sulastri. Trust remains the cooperative’s guiding principle.

The year 2020 was the hardest in the cooperative’s history. Severe floods inundated the store, destroying most of the merchandise. “The last flood cost us Rp70 million,” recalled Sri Sulastri. Refrigerators floated, and the office was left in shambles.

Before recovery could finish, the pandemic struck. Cooperative activities halted, the store grew quieter, and the annual meeting had to be postponed. By 2024, the cooperative’s surplus (SHU) was only Rp26 million, distributed directly into members’ savings accounts. “It was divided, but not in cash—it was too small, so just added into the books,” said Sutrisno.

Stalled by Regeneration

Currently, the cooperative is managed by seven board members. None of them work full time; they only receive a modest monthly honorarium. Those handling credit and bookkeeping earn Rp500,000 per month, while the others—including the chairwoman—receive only Rp300,000 per month.

These allowances are far below the minimum wage, yet no one complains. For them, it is a responsibility, not a job. “We’re just volunteers, walking from home to the office, sometimes even spending our own money,” said one board member (minute 15:32).

Most of the management are already elderly, with ages above 65. Still, they continue coming to the office on schedule, serving the few active members who remain.

Sri Sulastri admitted that regeneration is an unresolved internal issue. Every time the opportunity is offered, young people refuse to take on management roles. They are uninterested in the small honorarium and volunteer work. “If you offer Rp300,000, who would want it?” she said.

Yet, this cooperative was built on a spirit of kinship. In the past, anyone needing money to build a house, get married, or pay for schooling would come to the cooperative. “Back then, almost everyone here relied on the cooperative for their needs,” said Sulistiono. Today, however, people are more familiar with and often prefer online loans over visiting a cooperative.

Back then, almost everyone here relied on the cooperative for their needs.

The board members also expressed disappointment with the government. They feel they have never received support—whether in the form of training, incentives, or capital reinforcement. Even during the annual meeting, representatives from the local administration rarely attend. “The lurah (village head) should be the cooperative’s protector, but they never even show up,” Sulistiono said.

The cooperative had once hoped for state intervention, especially after suffering losses due to floods and the pandemic. But assistance never came. “At most, we just got a T-shirt during the cooperative’s anniversary celebration,” Sulistiono laughed. Even when they attended training sessions or forums, the outcomes were never sustainable.

Amid this disappointment, the government introduced a new program called Koperasi Merah Putih, designed to establish one cooperative in each subdistrict, complete with bank-funded capital loans.

The Bina Sejahtera board, however, views the program as good only on paper. Without proper oversight, they warn, cooperatives could become tools for manipulation and corruption—especially if run by people lacking sincerity. “If the management isn’t genuine, it won’t work,” said Sri Sulastri.

They stressed that building a cooperative is not the same as opening a shop. It requires time, commitment, and trust built over many years. “In our subdistrict, there was once a government-created cooperative. But it went bankrupt,” recalled Sulistiono.

Workers’ Weapon of Resistance

Although many cooperatives must struggle to survive today, in neighboring countries they still thrive and even dominate their markets. One example is Singapore’s National Trade Union Congress (NTUC), which manages consumer cooperatives that have grown into a massive supermarket network. It all began with a simple mission: to provide affordable prices for workers.

Today, NTUC dominates the retail market while allocating part of its profits for members’ education and welfare.

NTUC is listed among the 300 largest cooperatives in the world. It oversees sub-cooperatives such as NTUC FairPrice and NTUC Income, operating in retail and insurance respectively. The cooperative now has over 500,000 members, all of whom are also co-owners of its businesses.

NTUC FairPrice alone operates more than 291 stores across Singapore, ranging from convenience stores offering daily necessities to supermarkets and hypermarkets. Although FairPrice outlets carry different brand names, they all remain under the NTUC FairPrice umbrella.

The mechanism within NTUC follows the principle of a joint cooperative, where every member has equal voting rights in determining company policies.

At the Annual General Meeting (AGM/RAT), members can voice their opinions not only on policies but also on the Surplus Results of Operation (SHU) and its distribution.

What makes FairPrice unique is its SHU distribution system: the amount members receive depends on how much they shop at FairPrice outlets. In other words, the more a member spends, the larger their share of SHU.

The more a member spends, the larger their share of SHU.

The cooperative’s roots trace back to 1973, when Singapore’s national trade union NTUC established a retail cooperative in response to surging inflation. At the time, the price of essential goods soared, placing enormous pressure on low-income households.

Thus, NTUC Welcome was born—the forerunner of FairPrice—with a mission both simple and ambitious: to ensure that everyone, regardless of background, could access basic goods at fair prices.

From a single cooperative store, FairPrice gradually grew into a retail giant. Yet, it never abandoned its social roots. Today, FairPrice manages over 570 outlets across Singapore, ranging from standard supermarkets and premium stores to hypermarkets and 24-hour minimarts.

The cooperative has also expanded into food services through NTUC Foodfare and Kopitiam, underscoring its commitment to delivering comprehensive solutions for the daily needs of Singaporeans.

Profits Returned to the Community

What keeps FairPrice relevant and beloved by the public is not merely its extensive store network or service convenience, but the cooperative principles it consistently upholds. Profits are not distributed to a handful of shareholders as in private companies, but rather returned to society.

FairPrice’s business surplus is channeled into various social programs, including contributions to the Singapore Labour Foundation and the Central Co-operative Fund. Through this, FairPrice demonstrates that a company can remain competitive without sacrificing its social conscience.

When the Covid-19 pandemic struck, FairPrice not only ensured stable prices but also changed the way it served communities. It launched FairPrice on Wheels, mobile trucks delivering essential goods directly to neighborhoods that were hard to access or inhabited by vulnerable groups, such as the elderly. In times of crisis, their presence was felt not just as a store, but as a caring neighbor.

FairPrice’s social mission is also reflected in special discount programs for seniors and subsidies on essential goods. While other retailers use discounts to drive up sales volumes, FairPrice applies them as a form of economic intervention for those most in need.

FairPrice’s social mission is also reflected in special discount programs for seniors and subsidies on essential goods.

This does not mean their journey has always been smooth. FairPrice has faced criticism for certain products priced higher than competitors. On social media, some consumers questioned the cooperative’s commitment to affordability.

Management responded openly, explaining that their priority is quality, supply stability, and long-term partnerships with local producers. They deliberately avoid participating in price wars that could harm farmers or small suppliers.

Global e-commerce and aggressive discounting from new market entrants also pose real pressure. But instead of resisting the tide, FairPrice chose transformation. They strengthened their online services, developed a user-friendly e-commerce platform, and integrated their LinkPoints loyalty program to add more value for consumers.

In terms of environmental responsibility and sustainability, FairPrice also demonstrates awareness. They actively run programs to reduce single-use plastics, educate consumers on healthy lifestyles, and manage food waste in measurable ways. These efforts may not always be visible to someone walking through store aisles, but their impact is systemic.

Preparing to Go Global

FairPrice also recognizes that resilience cannot be built domestically alone. It has begun pursuing cross-border collaborations, such as its partnership in Vietnam, which launched Co.opXtra Plus—a hypermarket model combining modern retail with cooperative spirit. This expansion not only broadens their network but also spreads the message that cooperatives can succeed on the international stage.

In today’s increasingly competitive and capitalistic world, FairPrice serves as a reminder that retail does not have to be cold and purely efficient. It can have a friendly face, a caring heart, and a purpose greater than profit margins.

FairPrice proves that cooperatives are not an outdated model but a highly relevant economic system—especially when society demands fairness, solidarity, and equal access.

The story of FairPrice is not just about goods placed on shelves. It is about how a nation safeguards both the prices and dignity of its people. In every shopping cart pushed through a FairPrice outlet lies a long narrative of social struggle, courage to innovate, and commitment to collective welfare.

By Mukhlison, Rohman Wiboro, and Harits Arrazie