National Islamic finance requires digitalization and service innovation to maximize the potential of the large global market. This was conveyed by Deputy Chairman of the OJK Board of Commissioners Mirza Adityaswara at the Indonesia Islamic Finance Summit (IIFS) 2025 event organized by the Financial Services Authority (OJK) in Surabaya, East Java, Monday (3/10/2025).

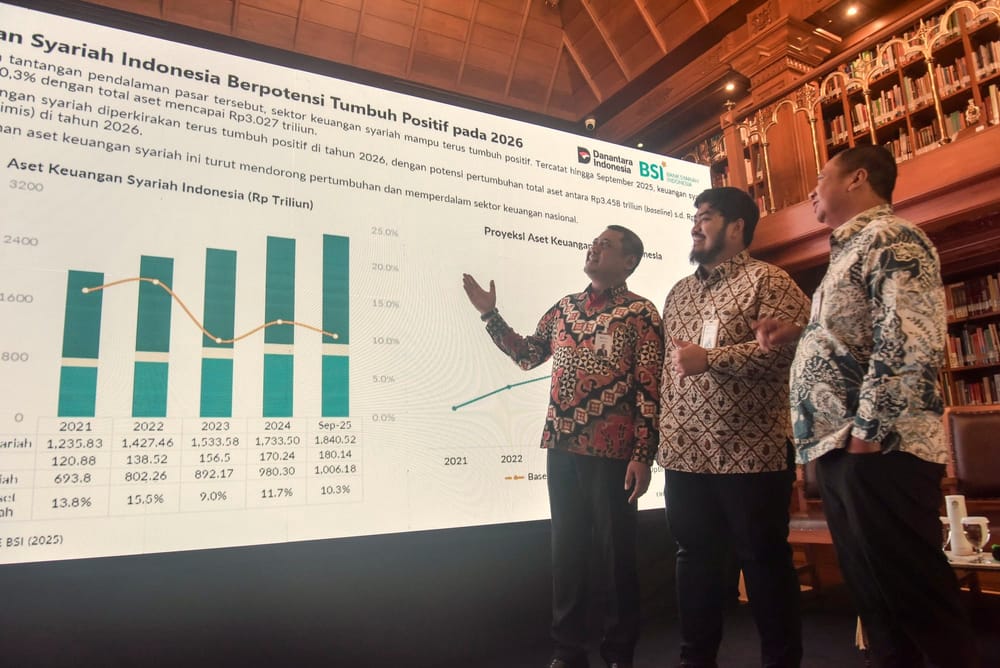

Based on data presented by OJK, as of September 2025, the total assets of Islamic financial services reached IDR 2,986 trillion, or the equivalent of 11.39% of total national financial assets.

Meanwhile, the Islamic capital market grew to IDR 1,832 trillion, followed by the assets of Islamic non-bank financial institutions, which also grew to IDR 178.6 trillion.

"This achievement cannot be separated from a number of challenges that still hinder the Islamic economy in Indonesia, such as the limited market share and economies of scale compared to conventional financial institutions. This means that a more aggressive strategy is needed to expand and enter the mainstream," said Mirza when delivering his keynote speech.

The limited market share that Mirza referred to relates to the Islamic financial literacy index, which has reached 43.4%, but the Islamic financial inclusion index has only reached 13.4%.

"In other words, the public is quite aware of Islamic financial service practices, but is not interested in using Islamic financial products or services," he said.

On the other hand, according to Mirza, limited capital has meant that the differentiation of Islamic financial business models has been unable to meet the needs of the community. In addition, there are limited human resources who are required to have dual expertise, namely modern financial practices and sharia law. In fact, both are crucial so that Islamic financial products are not only competitive, but also comply with sharia principles.

"OJK provides unique Islamic financial product guidance as an effort to deepen the market, such as cash wakaf link deposit (CWLD), salam contracts, as well as Syariah Restricted Investment Account, sharia securities, corporate sukuk, regional sukuk, and an online trading sharia system as an investment tool," he said.

Looking ahead, Mirza emphasized that strengthening the role of the Islamic financial industry continues to be pursued through synergies between Islamic financial institutions, Islamic social financial institutions, the halal industry, and UMKM. The hope is that with sufficient encouragement and a supportive ecosystem, sharia financing syndication will be able to reach the corporate segment.

The potential of philanthropy and waqf

Director of Social Finance at Bank Islam Malaysia Zikri Shairy acknowledged that capital is still one of the challenges of Islamic finance. However, he emphasized that a more difficult challenge is integrating Islamic social financial services with the conventional banking framework.

"Bank Negara Malaysia has included the Islamic financial economy in its 2033 blueprint. However, for that integration, we must ensure that the resulting business model does not replicate the working system of non-profit organizations. We must add value to the existing ecosystem," said Shairy.

Through various considerations, Bank Islam Malaysia chose and implemented the sadaqa house model as a way out, inspired by a speech by the late Dato' Abdul Halim Ismail (1939-2024), a pioneer of the modern Islamic financial system in Malaysia, when receiving the Global Islamic Finance Award in 2014.

With this model, the sharia bank becomes an enabler that receives and collects philanthropic funds to be distributed to marginal groups, orphanages and education through banking-like instruments under the name i-TEKAD. In addition to philanthropy, the bank also collects funds originating from zakat.

"I think the challenge lies in the courage to face the status quo, especially how regulators can be more open and design policies that suit aspirations. In addition, measuring the impact of policies must also determine the extent to which the distribution of funds has an impact on the local community," explained Shairy.

Expert Staff of the Department of Sharia Economics and Finance at Bank Indonesia Ali Sakti appreciated the story from the neighboring country, emphasizing that zakat and waqf are two important instruments in Islamic social financial services. This great potential, apart from being seen from the growth value, is also evident from the formation of the National Zakat Agency (BAZNAS) in Indonesia or Islamic Relief in the UK.

"We have one PNM Mekaar champion that serves up to 15 million customers, not to mention those based on customs such as Lumbung Piti Nagari in West Sumatra. However, what is rarely revealed from discussions about Islamic finance are the millions of people who receive the benefits," said Ali.

If efforts to collect waqf are pursued on an ongoing basis, continued Ali, the potential of more than 400,000 land waqf locations with an area of 57,000 hectares could become a large capital for Islamic financial services, not to mention cash waqf which can mobilize broader social financial services, thereby increasing the number of people served.

"The practice of zakat, waqf and anti-usury actually has a single message that is the core of the Islamic economy, namely don't leave a lot of resources idle," said Ali.

In an effort to maximize the potential of domestic waqf, BI is currently developing a Sharia Economic Development Fund (SEDF) which aims to integrate Islamic financial values with modern financial instruments such as sovereign wealth fund (SWF), professional governance, and strategic investment principles.

By maximizing waqf funds, SEDF will target investments in the form of state sukuk, strategic funding, and UMKM. Strategic funding that has been targeted includes the construction of the Wakaf Salman Hospital, Achmad Wardi Eye Hospital, and the empowerment of sharia microfinance.

"By optimizing the great potential of domestic waqf funds managed in such a way, various SEDF programs will increase the economic production capacity of the social sector, complementing the level of productive output that has also been produced by the private sector and the public sector," said Ali.

Back to the people

Through a Zoom teleconference, Professor of Islamic Political Economy at Durham University, Mehmet Asutay, reminded that in facing the challenges of global economic digitalization, Islamic finance must realize that innovation has a moral dimension, and every innovative decision must still be guided by the values of justice, balance, and the welfare of the people.

In his latest research, Prof. Asutay found that the deepening of the financial services sector and the expansion of financial services are increasing the risk of over-financialization. This means that money continues to circulate, but does not provide a real contribution to the benefit and socio-economic welfare of the people. In fact, the main function of financial services is to distribute resources.

"Islamic economics has a strong foundation that encourages innovation, renewal, and reform, and digital Islamic economics is part of it. For this reason, ethics and a sense of justice must be ingrained so that innovation increases justice and benefit, and has the aim of reducing inequality and promoting welfare," said Prof. Asutay.

In its application, digital economic innovation in Islamic finance takes the form of digital waqf platforms, zakat distribution with blockchain technology through Smart Sukuk, digital takaful, to micro-financing services and financial intermediation functions empowered by artificial intelligence (AI).

In addition to service automation, AI can also be used to check product suitability with sharia values. Thus, the competence of human resources can be fully directed at improving modern financial services, while the assessment of product alignment with sharia law can utilize AI algorithms.

"By aligning technology with the principles of ihsan, adl, and maqasid al-shariah, innovation in Islamic finance must serve the interests of humanity, not just for efficiency. True innovation lies not in faster technology, but in alignment with divine values, so that Islam can truly prove to be rahmatan lil-alamin," he concluded.